2025 MID-YEAR

Property loss adjusting

Report Objectives

This report aims to summarize the present metrics for our U.S. property programs, assess the landscape of the property claims market and benchmark our patterns against comparable industry research.

Unlike workers’ compensation, auto liability or general liability, property is not a monolithic product line. U.S. property consists of property loss adjusting and specialty services. Property loss adjusting contains five distinct product lines: catastrophe (CAT), high frequency low severity (HFLS), middle market, large loss and third-party administrator. Each of these has its distinct market, clients, competitors, pricing and service requirements. The specialty services division encompasses our forensic advisors/accountants, EFI Global (forensic engineering, environmental and fire experts), contents evaluators and building consultants. Sedgwick’s repair solutions, our direct repair network, auto damage appraisal and temporary housing are also significant and growing segments of U.S. property.

data parameters

Our practice team uses claims data to perform comparative analyses informed by their expertise and analytics. This report is based on data for U.S. claims only, though it is important to note Canada and Latin America are also significant pieces of our property Americas business.

Key observations

Sedgwick’s claim volume remained stable in mid-year 2025, even as the broader market saw a decline — driven by fewer major weather events and shifting policyholder behavior. As global policy changes and impacts to labor and materials started to drive up claim expenses, carriers continued leaning into tech-enabled solutions and artificial intelligence (AI) to streamline claims.

Our claim volume was steady through the first half of 2025

Within the broader market, we’re seeing a downward trend, primarily driven by a lack of significantly impactful weather events but also policyholder behavior.

Carriers are continuing to look for more efficient, cost-effective and technology-driven claim handling solutions to improve policyholder experiences and outcomes — both financial and performance. They’re also relying on AI to drive process efficiencies and agents to assist the claims handler in the decision-making process.

The cost of claims in both the personal and commercial space continued to rise.

We attribute this to geopolitical policy changes, including those related to tariffs and immigration, and the rising costs of materials and labor. Since it’s early and these policies are far from settled, we’ll continue watching for meaningful changes in our data.

Download a summary slide with these key observations.

REPORT CONTENTS

New assignments and pending claims

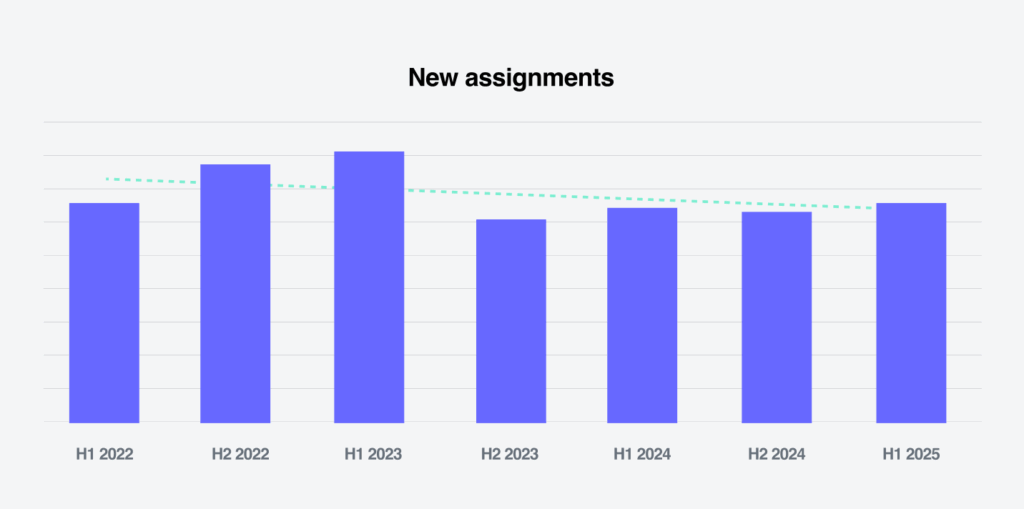

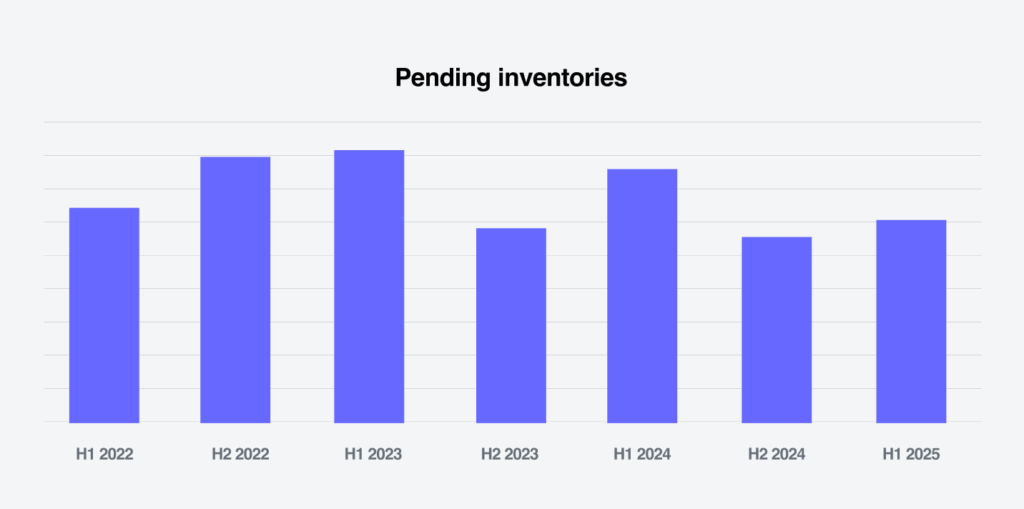

Overall, our property claim volumes held steady in what has been a downward trending market. Our diversification strategy — which includes an expanded suite of services, a proven service delivery model and a continued focus on the customer and their policyholders — has helped insulate us from this trend.

The below graphs depict new assignments as well as pending assignments (open inventory) since 2022. The large spikes in 2022 and 2023 reflect significant CAT activity experienced across the entire property claims landscape.

Industry claim trends have followed a similar trajectory as our U.S. property book of business, except for the second half of 2024 and beginning of 2025. According to Verisk’s Quarterly Property Report January-March 2025, Q1 2025 brought a 7% reduction in Verisk’s overall claims since last year, which already saw a 15% reduction from 2024. Verisk attributes the continued downward trend in their claim volume to the lowest non-CAT claims count in five years and the second-lowest catastrophe claims assignments since before the pandemic.

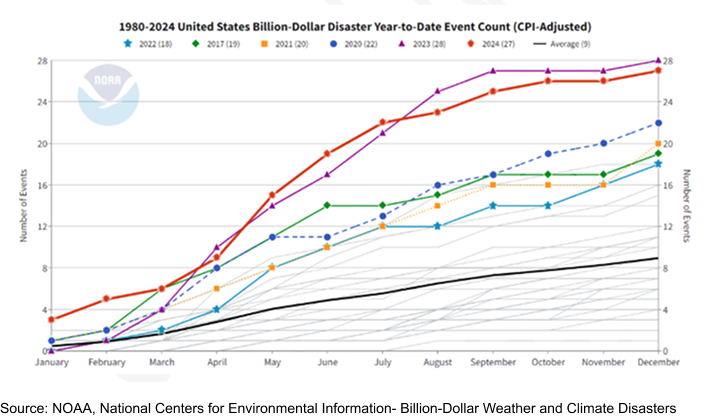

Weather

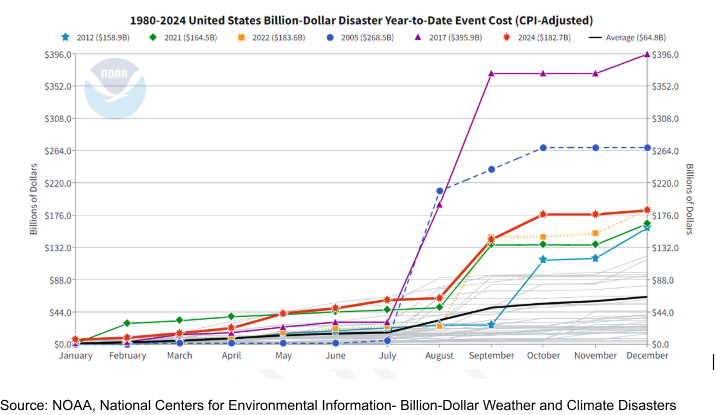

Weather continues to be volatile, and this variability remains a decision-making factor within the property claims space. The National Oceanic and Atmospheric Administration (NOAA) produces data on billion-dollar weather events that continues to be the industry-recognized measure, irrespective of claim volume and cost.

As represented in the first graph below, since 1980, there’s been an average of nine billion-dollar weather and climate disasters per year (data has been adjusted for inflation using the Consumer Price Index or CPI). Over the last five years, there’s been an average of 23 billion-dollar events — an alarming increase. Any one of these storms has the potential to impact the U.S. with similar claims volume scenarios to 2005 or 2017.

The second graph from NOAA shows the average cost per billion-dollar event since 1980 (costs are CPI-adjusted). This data demonstrates the volatility and unpredictability of weather and CATs within the property space. 2023 and 2024 saw a similar number of billion-dollar events, but there is a significant disparity in the dollars incurred between those two years due to the magnitude of events.

The unpredictable nature of CAT impacts year over year — coupled with the long-term trend of increasing severity due to climate change — requires claims leaders to be prepared. A carefully planned strategy should include:

01

Strong data analytics outlining potential catastrophe scenarios overlaid against policies in force

03

Continuous review of new technologies to improve efficiency

02

Key partnerships in place including workflows and processes tested and confirmed

04

Emergency “break glass if needed” plan

Policyholder behavior

Insurance premiums and deductibles are rising sharply, even for policyholders who haven’t filed claims, largely due to the growing impact of catastrophic events. According to the Consumer Federation of America’s Overburdened Report, homeowners’ policies have increased 24% over the past two years — reflecting how widespread risk drives up costs for the entire market.

This, coupled with an increase in wind and other deductible changes instituted by carriers, has made policyholders keenly aware of claim event impact. According to a survey conducted by Guardian Services: Nearly 1 in 4 homeowners admitted they’ve avoided filing an insurance claim because they were afraid their home’s condition might trigger an inspection or even a denial.

These factors have led to fewer claims reported and policyholders seeking alternative methods other than insurance to fund their repairs.

Impact of stricter immigration policies and tariffs

The shift in U.S. federal leadership has resulted in updates to existing policies and the development of new ones. While the full impact can’t be quantified yet, these changes will influence claim costs.

Immigration policy changes could have a significant impact. According to Verisk’s Quarterly Property Report January-March 2025, immigrant workers made up 26% of the construction workforce in 2023 — significantly higher than their share in the overall U.S. labor force.

In addition, core personal and commercial construction materials are potentially susceptible to impacts of new tariffs. Any increase in cost to these materials beyond the standard expected increase could substantially increase claim loss expense and severity.

Again according to Verisk’s Quarterly Property Report January-March 2025, in 2024, 28% of the softwood lumber used in the U.S. was imported. In 2023, 24% of all concrete was imported. Gypsum (used in drywall) is another commonly imported material. Lumber, concrete and gypsum primarily come from Canada, Mexico or China, so new tariffs on goods from those countries are expected to cause volatile pricing and disrupt supply chains.

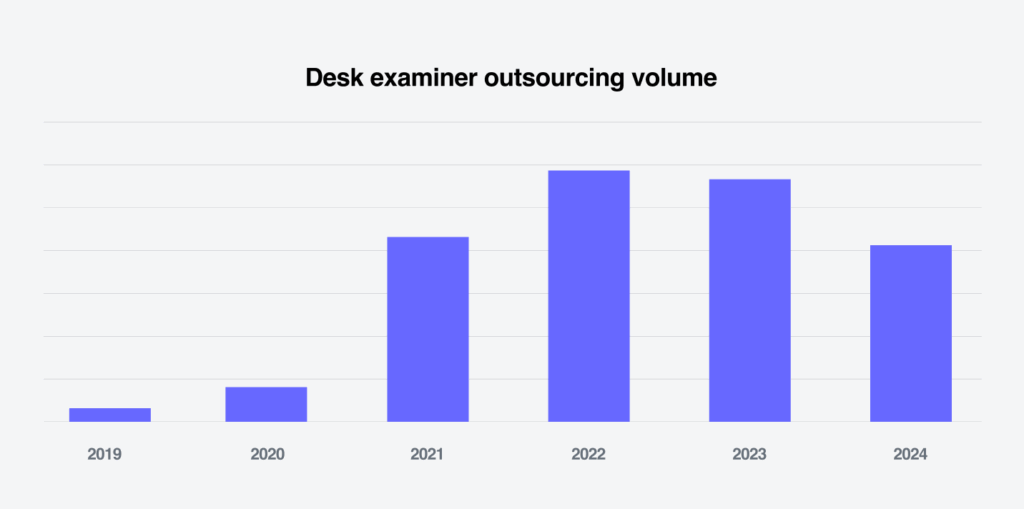

Desk examiner outsourcing

The success of remotely adjusting small- to mid-sized auto damage claims during and after COVID-19 has driven carriers’ appetite for personal and commercial desk adjusting.

We’ve seen growth and sustained demand for it since 2019, as the graph below shows (2022 and 2023 include significant CAT activity).

The growing market requirement for accurate, efficient technological capabilities and a single-source damage assessment solution has proved challenging compared to the auto space. Earlier this year, we released Digital Adjust Pro to meet these market demands.

Our new solution provides carriers with an outsourced desk examiner resource to support the claim — along with our array of property damage assessment capabilities, including auto-adjudication, remote scope, inspection only and on-site adjustment. Digital Adjust Pro combines all services seamlessly and leverages the latest in claims automation — made possible through our substantial investments in technology. By using our new solution, carriers have realized improved outcomes, lower costs and a best-in-class policyholder experience.

Carriers will continue to outsource to partners due to the volatile nature of claims. While traditionally the focus has been on field resources, there will be increased utilization of desk examiners in the future.

AI and data

Property claims are becoming increasingly shaped by AI. Client discussions and internal development have stressed the focus of AI in three key areas: process efficiency, accuracy and customer experience. Specific examples include:

01

Claims triage/image recognition

02

Fraud detection

03

Damage assessment/image recognition

04

AI customer chatbots (including personalization)

05

Workflow automations

These initiatives are complex, and many companies have focused on creating a comprehensive AI strategy within their organizations. This strategy should include a clear understanding of ultimate goals for the organization and a concise process for prioritization so that the most impactful AI use cases are identified, developed and delivered first.

AI is also a powerful tool for companies to analyze the data, both unstructured and structured, that already exists within their organization, so they can use that information to improve.

Unstructured data — such as emails, documents/reports and photographs — is in an undefined format that’s harder to analyze. Structured data — such as data captured in a claims system and stored in a database — is in an organized, predefined format. Our property adjusters enter significant amounts of both kinds of data, whether they’re writing unstructured reports or entering structured data into fields in our claims system.

In 2024, we launched a proof-of-concept project that leveraged AI to analyze the data entered by our property adjusters to unlock valuable insights from it. As part of the project, we used Sidekick (our AI tool) to build basic AI prompts that reviewed a subset of reports for key data points and findings. Prior to AI, there was no way to extract rich data like this without reading and analyzing thousands of reports manually.

The proof of concept resulted in a tremendous amount of learning and momentum into how we can enhance transparency and improve both colleague and customer experiences. Below is a small sampling of results from the project.

Future considerations

Although new assignment and pending claim counts remained steady within our property book of business, that is not the story industry wide. Our diversified portfolio of service offerings has helped insulate us from the ongoing prolonged downturn in claims activity. Verisk reported a 7% drop in claims year over year, on top of an overall 15% decrease from 2023.

A lack of significantly impactful weather events and changes in policyholder behavior appear to be key drivers for this slowdown in reported claims. As reported by NOAA, billion-dollar storm activity remains high however, so the volatility in weather should continue to be a primary focus, along with being prepared.

Another key concern is the uncertainty around claim costs stemming from immigration and tariff policies. It remains unclear the level of impact these policy changes will have, but the cost of labor and materials will rise due to these changes. These increases will have downstream impacts throughout the property claims ecosystem, and we should be considering those impacts now.

Finally, changes to claims handling processing like desk outsourcing and AI are here to stay.