Download a summary slide with these key observations.

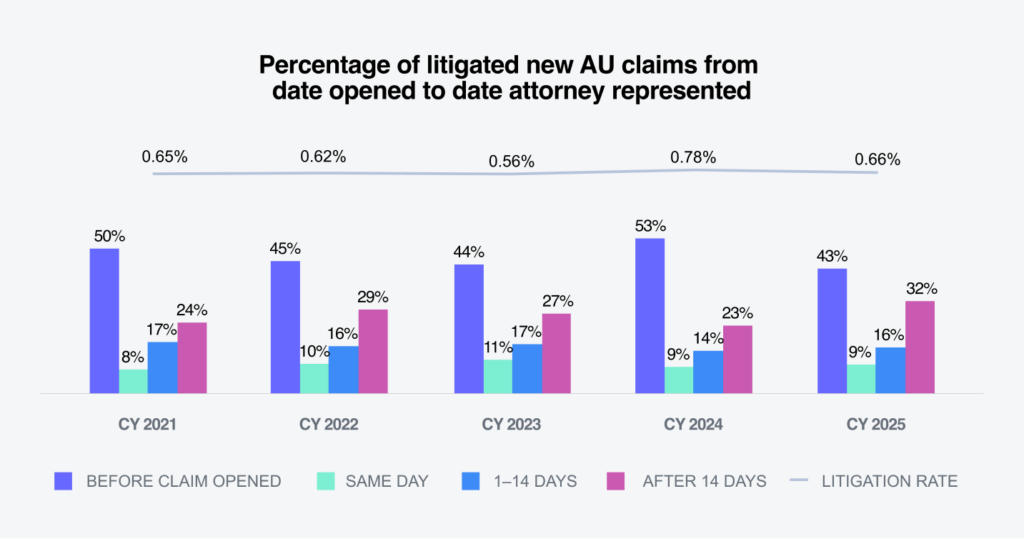

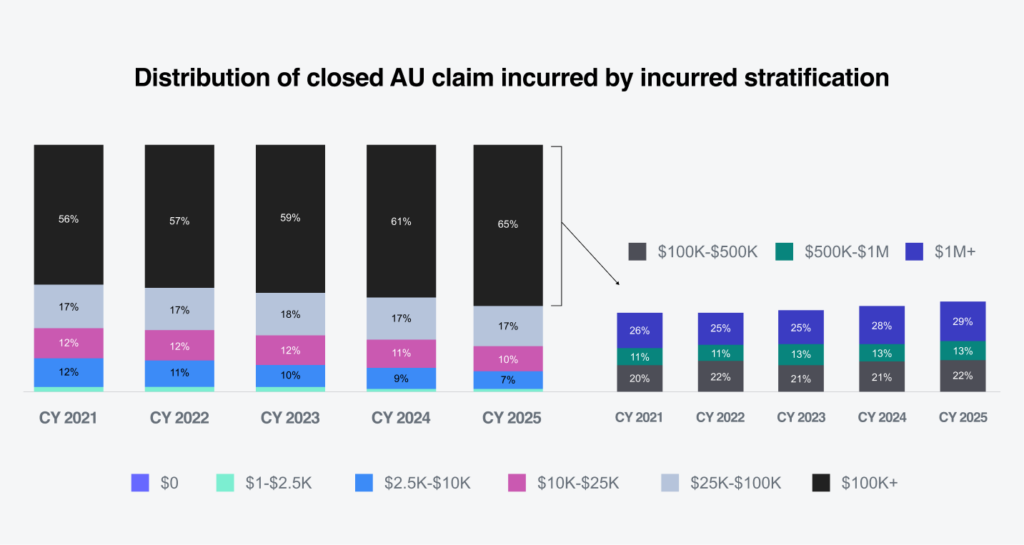

For companies and risk managers, these trends require a strategic shift. Traditional claims management approaches focused primarily on closure speed and expense control are no longer sufficient. Instead, organizations must emphasize early severity identification, rapid escalation protocols for attorney-involved claims and venue-aware defense strategies. Greater investment in analytics, predictive modeling and closer collaboration among claims, legal and risk teams is critical to identifying high-risk claims sooner and intervening before positions harden and costs escalate.