2025 YEAR-END

Property loss adjusting

Report Objectives

This report aims to summarize the present metrics for our U.S. property programs, assess the landscape of the property claims market and benchmark our patterns against comparable industry research.

Unlike workers’ compensation, auto liability or general liability, property is not a monolithic product line. U.S. property consists of property loss adjusting and specialty services. Property loss adjusting contains five distinct product lines: catastrophe (CAT), high frequency low severity (HFLS), middle market, large loss and third-party administrator. Each of these has its distinct market, clients, competitors, pricing and service requirements. The specialty services division encompasses our forensic advisors/accountants, EFI Global (forensic engineering, environmental and fire experts), contents evaluators and building consultants. Sedgwick’s repair solutions, our direct repair network, and our auto damage appraisal and temporary housing services are also significant and growing segments of U.S. property.

data parameters

Our practice team uses claims data to perform comparative analyses informed by their expertise and analytics. This report is based on data for U.S. claims only, though it is important to note Canada and Latin America are also significant pieces of our property Americas business.

Key observations

At a glance, today’s property claims environment is shaped less by isolated catastrophe events and more by how risk behaves over time, across geographies and by peril. Success is defined by scaling smoothly, controlling severity and delivering consistent outcomes as conditions evolve.

Risk shift

More frequent, dispersed events

Claim reality

Severity stays elevated even when volume softens

Operating response

In-house capacity and strategic partner support

Enablers

Technology and expert judgment

Outcome

Desired operating state

The implications for claims operations:

Risk is shifting, not declining.

Losses are increasingly driven by event frequency, geographic dispersion and cumulative impact, rather than a limited number of peak catastrophe events.

The peril mix is changing.

Non‑hurricane events now account for a growing share of claim activity, expanding exposure beyond traditional high‑risk definitions and spreading losses across more regions and seasons.

Claim volume does not equal financial exposure.

Even when new claim intake moderates, severity pressures remain elevated, driven by labor constraints, materials cost volatility, coverage dynamics and post‑loss friction.

Technology and expertise together drive outcomes.

Digital and AI‑enabled capabilities support speed, visibility and consistency, while experienced judgment remains essential for complex and high‑severity losses.

What this means for insurers and risk managers:

Plan for year-round volatility.

Prepare for clustered activity and localized surges, not just traditional peak catastrophe seasons.

Actively manage severity.

Align governance, escalation paths and expert resources to high‑complexity and total loss claims, where outcomes are most sensitive.

Build flexible capacity.

Use scalable operating and partner models that can expand quickly while maintaining control, consistency and customer experience.

Use technology to enable, not replace, decisions.

Apply automation and AI to improve segmentation, visibility and cycle time, while preserving expert judgment.

Download a summary slide with these key observations.

REPORT CONTENTS

The evolving property risk landscape

Escalating challenges in property claims

Elevated event frequency and geographic dispersion continue to translate into greater claim complexity, driving increased severity pressure and the need for stronger governance across property claims.

Market conditions

- Increased event frequency

- Broader geographic spread

- Repeated and clustered disasters

Claim complexity

- More complex losses

- Unpredictable scenarios

- Intensive coordination required

Operational impact

- Longer cycle times

- Higher severity costs

- Increased oversight and controls

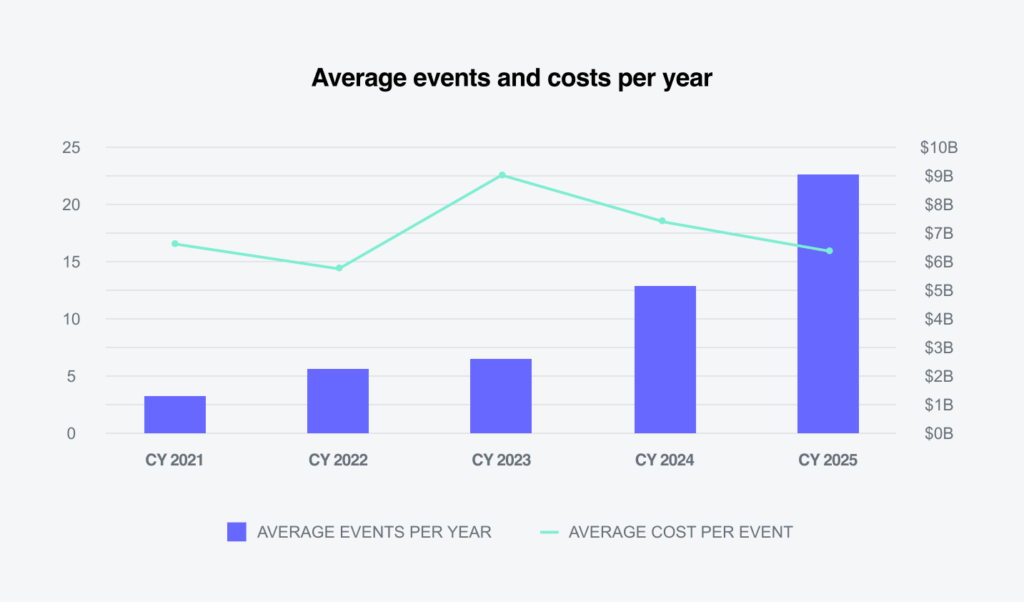

Claim frequency has increased as per event severity moderated

Over the past four decades, the frequency of billion‑dollar weather and climate events has increased steadily, reaching historically high levels in recent years. At the same time, the average cost per event has leveled off from earlier peaks.

This divergence reflects a fundamental shift in how losses occur. Rather than being driven primarily by a small number of extreme catastrophes, loss activity is increasingly shaped by recurring, midsized events that cause less damage individually, but collectively produce sustained disruption throughout the year.

Why this matters now: Higher frequency combined with broader geographic dispersion is increasing volatility, reducing predictability and raising cumulative exposure, even in years without major hurricanes.

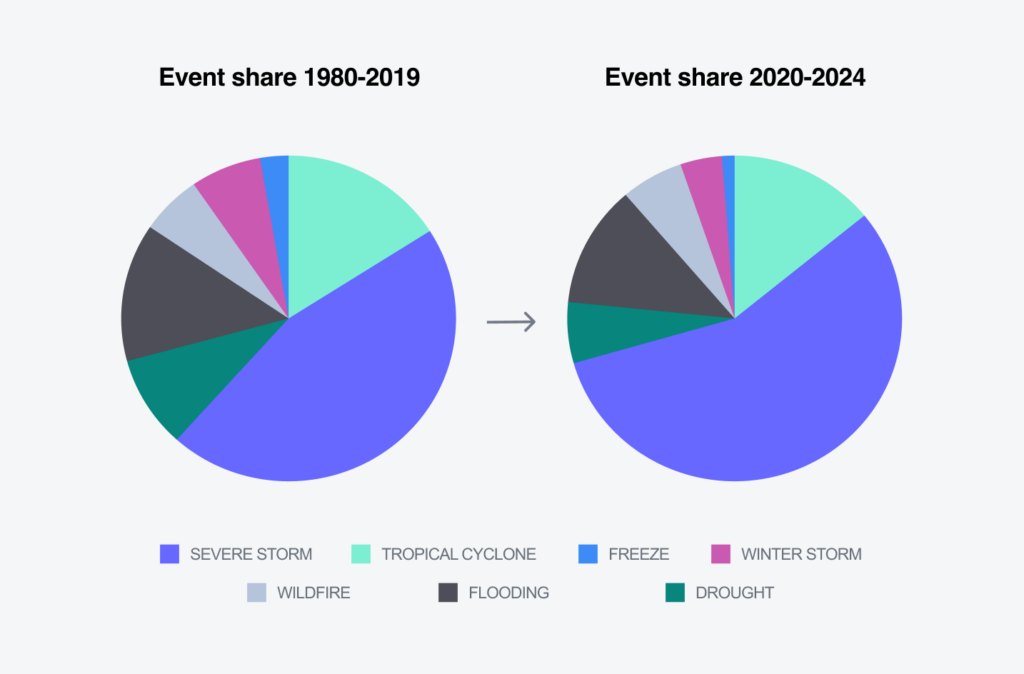

The peril mix has shifted

The composition of billion‑dollar weather events has shifted over time. While hurricanes continue to generate some of the largest individual losses, the overall event profile has moved toward higher‑frequency, non‑hurricane perils.

In recent years, severe convective storms have emerged as the primary driver of event activity. From 2020 to 2024, severe storms accounted for about 60% of all billion‑dollar weather events, up nearly 15% from prior years.

As a result, industry exposure is no longer concentrated around a limited number of peak hurricane events. Instead, it is increasingly shaped by frequent, geographically dispersed events that accumulate risk across regions and seasons.

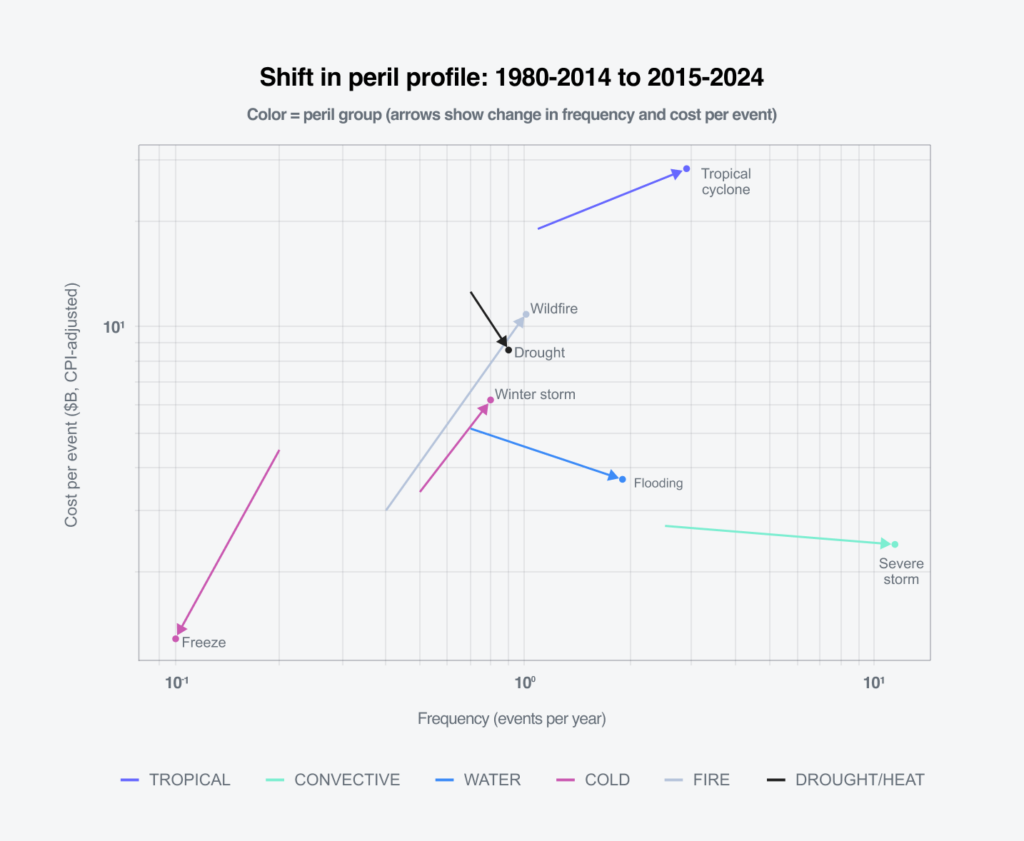

Risk is not just increasing — it is changing shape

The shift in property risk is not only about more events or a changing peril mix. It reflects how losses are forming and behaving across perils. As activity spreads across regions and seasons, insurers are seeing greater variability in coverage outcomes, repair pathways and recovery timelines. That variability is a key driver of claim complexity.

Different perils are evolving in distinct ways, further complicating the risk landscape.

- Severe storms continue to trend toward higher frequency with lower cost per event, driving cumulative disruption.

- Flooding is occurring more often outside traditionally mapped risk zones, frequently resulting in uninsured or underinsured losses.

- Wildfires increasingly result in total loss claims, with recovery timelines affected by rising reconstruction costs, limited labor availability and insurance-to-value gaps.

- Winter storms remain a recurring source of regional loss spikes, adding variability to annual patterns.

What this shift signals: More losses are occurring outside traditional high‑risk definitions, increasing complexity and recovery friction, even as average loss per event declines.

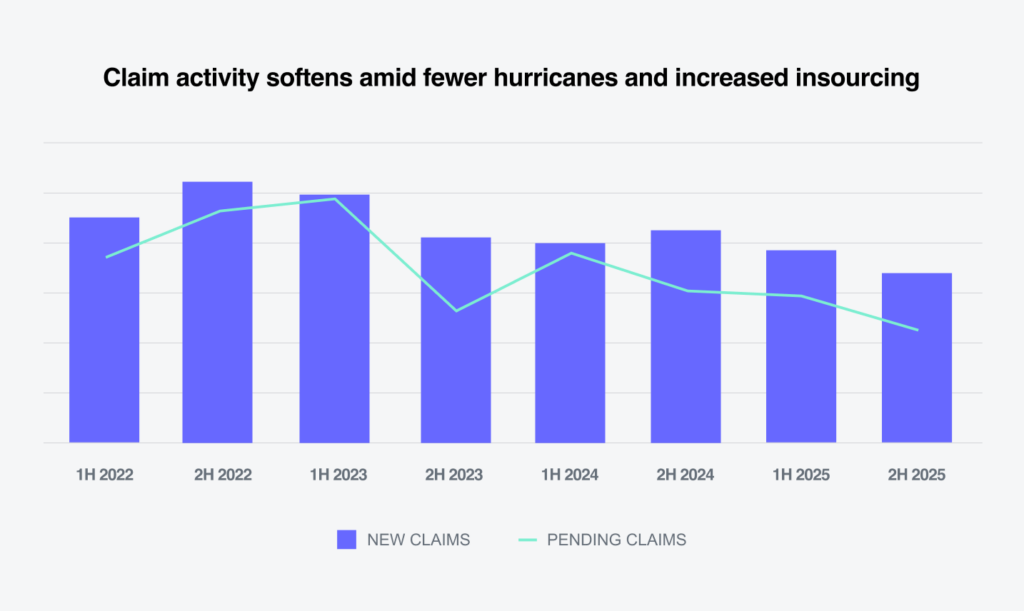

Translating market conditions into claim activity

The evolving property risk environment is not translating into claim volume in a linear or predictable way. Recent declines in claim counts reflect market behavior and claim formation dynamics, not a reduction in underlying exposure.

Sedgwick’s U.S. property loss adjusting data shows a decline in new claim intake alongside a reduction in pending inventory. This trend aligns with a period characterized by fewer high‑severity hurricane events, continued underwriting discipline, higher deductibles and shifts in policyholder behavior. Together, these factors have limited the number of losses that convert into insured claims, even as physical damage continues to occur.

At the same time, changes in the peril mix have introduced a structural constraint on claim formation. Events such as inland flooding and wildfire losses increasingly fall outside traditional coverage structures or exceed insurance‑to‑value assumptions. In these cases, damage occurs without corresponding adjusting activity, masking underlying exposure and dampening apparent demand.

As a result, lower claim volumes should not be interpreted as reduced risk. Instead, they reflect a disconnect between physical loss and insured claim generation, driven by coverage gaps, deductibles and evolving peril behavior. When conditions shift — through renewed hurricane activity, regional clustering of events or changes in underwriting posture — claim volumes and operational demand are likely to respond quickly.

These conditions represent a cyclical pause rather than a structural shift in the property claims environment. Recent softening in claim intake reflects a combination of short‑term factors, including hurricane activity, underwriting posture, policyholder behavior and near‑term capacity alignment, rather than a permanent change in exposure or volatility. As event patterns recluster, coverage dynamics evolve or severity pressures compound, operational demand can re-accelerate quickly. This reinforces the importance of maintaining scalable operating models and access to specialized expertise that can flex alongside internal teams as conditions continue to evolve.

Claims impact: Periods of eased volume represent a cyclical pause, not a structural shift. They create an opportunity to refine governance, strengthen segmentation and reinforce readiness, positioning organizations to scale smoothly when claim activity accelerates.

Why severity remains elevated

Severity driver stack

Property claim severity is not driven by a single factor — it reflects stacked pressures across labor, materials, coverage adequacy, complexity, event type and post-loss conditions.

01

Post loss friction

Contractor availability, negotiation cycles, dispute timelines

03

Claim complexity

Specialty structures, code upgrades/ordinance

05

Materials and supply constraints

Volatility in materials, delays extending ALE/rental

02

Event type

Total loss versus repair, fire spread/flood depth

04

Coverage adequacy

Underinsurance, limits/gaps discovered mid-claim

06

Labor availability and cost

Skilled resource shortages, overtime premiums

01

Post loss friction

Contractor availability, negotiation cycles, dispute timelines

02

Event type

Total loss versus repair, fire spread/flood depth

03

Claim complexity

Specialty structures, code upgrades/ordinance

04

Coverage adequacy

Underinsurance, limits/gaps discovered mid-claim

05

Materials and supply constraints

Volatility in materials, delays extending ALE/rental

06

Labor availability and cost

Skilled resource shortages, overtime premiums

Even as claim volumes soften, claim severity remains elevated across the property landscape. Severity reflects layered pressures that accumulate throughout the claim lifecycle, including labor availability and cost, materials and supply constraints, coverage adequacy, claim complexity, event characteristics and post-loss conditions.

- Labor availability and cost continue to extend repair timelines and increase settlement pressure, particularly in skilled and specialty trades.

- Materials and supply constraints introduce pricing volatility and delays that compound severity, even in moderate losses.

- Coverage adequacy, including higher deductibles, limits and uncovered perils, creates friction between damage and recoverable amounts.

- Claim complexity increases coordination demands in multiparty, specialty and total loss scenarios.

- Event type, such as total loss versus repairable damage, materially influence claim duration and outcome variability.

- Post-loss conditions, including contractor availability and rebuild timelines, often determine ultimate claim outcomes.

These severity drivers are further compounded by social inflation, which acts as a multiplier rather than a primary cause. In higher‑severity or prolonged losses, elevated expectations and increased dispute activity can extend resolution timelines and intensify post‑loss friction.

Rather than driving a single operating response, these compounding pressures have pushed the market toward more adaptive claims models, in which capacity, expertise and technology are deployed differently depending on conditions.

Market response

Adapting operating models and enabling technology

Recent market conditions have not driven carriers toward a single, uniform operating response. Instead, they have increased the need for flexibility, with claims strategies increasingly shaped by current event activity, available internal capacity and the complexity of reported losses.

During quieter periods, carriers are handling a larger share of claims internally, supported by tighter governance, clearer escalation paths and closer oversight of outcomes. When activity accelerates — through catastrophe events, regional clustering or cumulative disruption — carriers must be able to scale quickly, deploying surge capacity and specialized expertise without sacrificing control or customer experience.

This shift has moved the market away from static resourcing models and toward adaptive claims operations, in which capacity is aligned to claim complexity rather than volume alone.

ADAPTING TO MARKET CONDITIONS

Quiet periods

- Insourced select low severity claims

- Outsourced high complexity claims

- Tighter oversight

Active periods

- Surge capacity support

- Scalable claim solutions

- Expertise on demand

SEDGWICK’S TECHNOLOGY AND AI SOLUTIONS

Digital intake and triage

AI-supported damage assessment

Workflow automation

AI-enabled fraud identification

AI-driven customer experience

Sedgwick empowers clients with advanced technology to deliver scalable claim solutions in any market environment.

Technology and AI as the connective layer

Technology and AI play a critical role in enabling this adaptability. Rather than serving as standalone strategies, they function as connective layers, linking market conditions, operating decisions and claim outcomes.

Across operating environments, technology is increasingly used to:

- Support digital intake and early triage, improving segmentation at the outset

- Assist with damage assessment, including remote and AI‑supported tools

- Enable workflow automation, reducing administrative friction and cycle time

- Enhance fraud identification, particularly in repeat or pattern‑driven losses

- Improve customer communication and transparency throughout the claim lifecycle

These capabilities allow organizations to accelerate resolution where complexity is low, while preserving experienced judgment for higher severity, nonstandard or total loss scenarios.

Despite continued investment in automation and analytics, property claims remain inherently variable. Coverage interpretation, severity evaluation and recovery outcomes continue to depend on experienced professionals, particularly as losses increasingly fall outside historical norms.

Operational implication: The market response is no longer about choosing between in‑house or outsourced models, or between human expertise and technology. It is about continuous adaptation — using the right mix of internal capacity, trusted and scalable partners, and enabling technology to match conditions as they evolve.

Future considerations

Near-term expectations

The U.S. property claims environment is not entering a period of reduced risk. While recent conditions have been shaped by fewer major hurricane events and disciplined underwriting, the underlying drivers of claim frequency, severity and complexity remain firmly in place.

Looking ahead, claim activity is expected to remain uneven, with quieter periods followed by rapid shifts driven by weather patterns, regional clustering of events and changes in market behavior. Non‑hurricane perils are likely to continue driving cumulative disruption, even in years without a defining catastrophe season.

At the same time, the factors contributing to elevated severity are expected to persist. Labor availability, materials cost volatility, coverage dynamics and post-loss friction will continue to influence outcomes, particularly in complex and total loss claims.

Periods of lower claim intake should not be viewed as reduced financial exposure. Instead, they present an opportunity for carriers to strengthen governance, refine segmentation and reinforce operational readiness ahead of the next inflection point.

Positioned for what comes next

The property claims landscape is entering a period of more dynamic risk, not greater stability. Organizations best positioned to succeed will be those that remain adaptable as conditions change, align resources to complexity rather than volume, and invest in capabilities that perform across both quiet and active periods. This places increased emphasis on:

- Flexible operating models

- Trusted, scalable partners that can flex alongside internal teams

- Technology that supports speed and insight without replacing professional judgment

Closing perspective: In today’s property environment, success is defined less by forecasting precision and more by readiness — the ability to scale smoothly, apply expertise where it matters most and deliver consistent outcomes as conditions evolve.

Citations:

- NOAA. National Centers for Environmental Information. U.S. Billion-Dollar Weather and Climate Disasters. 2025.

- Sedgwick. Internal claims data and operational analytics, 2020–2025.

- CoreLogic, LexisNexis Risk Solutions and other third-party property risk intelligence sources.

PAST REPORTS

2025 YEAR-END